From April 4-6, I competed in the University of Chicago’s Econometrics Game in a group with three of my classmates. In this competition, teams are given 12 hours with a dataset to devise and answer a question of economic importance.

We won 2nd place!

Below, you can find this year’s prompt as well as my group’s paper. I hope you find this interesting!

Prompt: Your task is to use the IMF PortWatch daily port activity data to identify and estimate the causal effect of an event of your choice on trade flows. The port activity data and trade estimates can be downloaded from the IMF Portwatch website, which includes a full description of the variables and trade estimates in the .csv file. You may use this or any other publicly available data to answer your question. We recommend you open the data using fread() in the data.table package in R.

Part 2: How does the Federal Reserve manipulate interest rates?

Welcome back! To start off blunt, the Federal Reserve answers this question on its website. They state,

“When necessary, the Fed changes the stance of monetary policy primarily by raising or lowering its target range for the federal funds rate, an interest rate for overnight borrowing by banks. Lowering that target range represents an “easing” of monetary policy because it is accompanied by lower short-term interest rates in financial markets and a loosening in broader financial conditions. This action may be needed if the economy is sluggish or inflation is too low. Raising the target range represents a “tightening” of monetary policy, which raises interest rates and may be necessary if the economy is overheating or inflation is too high.”

Great. Here we introduce what’s called the Federal Funds Rate (FFR), the interest rate for overnight borrowing by banks. This is a range of possible interest rates at which banks charge for taking 1-day loans from each other. Banks hold ‘reserves’ at the Fed and get paid a certain amount of interest on these reserves, coined the Interest on Reserve Balances (IORB). The IORB is the Fed’s primary tool for guiding the federal funds rate. So, the Fed sets the IORB which influences the FFR. Boom. The Fed created the 1-day interest rate.

Crucially, the Fed doesn’t need to do much to ‘give’ private banks reserves. In fact, the Fed creates reserves electronically out of thin air. They create these reserves and create the money they use to pay interest on these reserves. That’s a lot of power. For this reason, banks view the Federal Reserve as the safest financial institution to hold money/reserves. The Federal Reserve will never default or run out of money because they can just create more! Pretty neat.

Although the Fed predominantly uses the IORB to set the FFR, it uses other tools as well. One such tool is called Open Market Operations (OMO). This refers to the Fed buying and selling U.S. Treasury securities. When the Fed buys U.S. bonds, they typically buy bonds from primary dealers with reserves. Primary Dealers refer to the trading counterparties of the New York Fed in its implementation of monetary policy, which typically include large financial intermediaries such as J.P. Morgan, Goldman Sachs, etc. A full list of primary dealers can be found here. When the Fed purchases U.S. Treasury securities, these financial intermediaries have more reserves to go around, thus reducing the relative value of reserves (banks are less willing to pay for reserves) and reducing the FFR.

Let’s summarize. So far, we know that the Federal Reserve influences the 1-day interest rate (FFR). They do this by directly setting the interest rate on reserves (IORB) and by buying and selling U.S. Treasury securities (OMO).

Great! But we aren’t just concerned with the 1-day interest rate. What about 1 month? 1 year? 10 years? 30 years? Although the Federal Reserve does not directly set these interest rates, they have strategies for manipulating them.

As briefly mentioned earlier, short-term interest rates strongly influence longer-term interest rates. Think about it. Suppose you continually invest in the 1-day interest rate for 30 days. You alternatively could have invested in a 30-day interest rate. The 30-day interest rate, then, should be roughly on par with the 1-day interest rate. If the expected 1-day interest rates are significantly higher than the 30-day rate, everyone will forgo the 30-day investment for the 1-day investment for 30 days, driving up the price of 1-day investments and reducing the rate. Conversely, if the 30-day interest rate was significantly higher than the expected 1-day rates for 30 days, people would forgo the 1-day investment and bid up the price of the 30-day investment, reducing its yield.

This phenomenon of short-term rates influencing long-term rates is called the Expectations Hypothesis of the Term Structure of Interest Rates (aka the Expectations Hypothesis). Long name, I know. But this generally shows us how the Federal Reserve also controls long-term interest rates. If investors believe the Federal Reserve will set a certain FFR over 10 years, the 10-year Treasury bill should roughly be equal to the average expected FFR over 10 years.

In practice, the Federal Reserve often intentionally signals something about the future to manipulate long-term interest rates. This strategy is called forward guidance: where the central bank tells the public about the likely future course of monetary policy. If investors believe the central bank, they will price or reprice long-term interest rates accordingly.

One other way the Federal Reserve influences long-term interest rates is through Quantitative Easing (QE). QE refers to the central bank purchasing long-term securities like government bonds, mortgage-backed securities, or corporate bonds. In doing so, they bid up the price of these securities which mechanically lowers the yield. This serves as a stimulative policy that injects money into the economy and decreases the interest rate. Notably, the central bank can also ‘reverse’ this policy with Quantitative Tightening (QT). Predictably, this refers to the central bank selling long-term securities, decreasing their price and increasing the interest rate.

QE and QT are relatively recent phenomena, first piloted by the Bank of Japan in 2001. The Federal Reserve first used it in 2008 in response to the Global Financial crisis, and is currently using QT as a tightening tool right now (don’t hate on the Wikipedia citation)!

That was a quick crash course on how the Federal Reserve manipulates interest rates! They create reserves out of thin air, pay interest on those reserves, and use these reserves to buy & sell securities to change interest rates. They also use future expectations of rates to change long-term interest rates. Amazing! But how exactly do interest rates flow through to the economy? Do the nominal rates matter? Or, do the rates adjusted for inflation matter? Why do different interest rates differ? I’ll answer all of these in my next section: How interest rates affect the economy!

In my foundational macroeconomics course, the answer was simple: Monetary policy is when the Federal Reserve sets the short-term interest rate. The expectation of short-term interest rates over time comprises longer-term interest rates. Thus, the Federal Reserve determines short-term and long-term interest rates.

Why do interest rates matter? Well, rates influence the amount of borrowing and spending in an economy. If rates are high, they are said to be ‘restrictive’ in that they limit excess borrowing and spending as the cost of borrowing is high. If rates are low, they are ‘stimulative’ as they incentivize more borrowing and spending.

Great! Here’s a question, though: Why don’t we keep rates low? That is, why doesn’t the Federal Reserve keep rates at 0? Or, even better, why don’t they set rates at negative levels? That way, it’s super attractive to borrow money, so we’ll have a lot of borrowing and spending which is good for the economy! Well, one consistent theme in life is that too much of a good thing is a bad thing. There are healthy levels of spending, and there are unhealthy levels of spending. If an economy borrows and spends without a commensurate increase in the production of goods and services, a phenomenon called ‘inflation’ occurs. And, if borrowing and spending vastly outpace production, we’ll see something called hyperinflation, where money is so devalued it essentially becomes worthless. Some examples of hyperinflation include Germany after World War I, Zimbabwe in 2008, and Hungary in 1946. Fun fact: Hungary experienced 13,600,000,000,000,000% inflation in a month! Makes 5% annual inflation seem pretty tame, right? (Be sure to search “Zimbabwe hyperinflation” for a visual depiction of what this looks like!)

In sum, the Federal Reserve, or any central bank for that matter, uses interest rates to balance spending and inflation. In fact, the Federal Reserve has a ‘mandate’ to “pursue maximum employment and price stability”. In other words, they seek to keep inflation manageable while supporting borrowing and spending such that firms are healthy enough to hire people looking for jobs. This is great! Now, at a broad level, we understand what the Federal Reserve does. It plays an important role in managing inflation and keeping the labor market healthy.

But, how exactly does the Fed do this? How do they set the interest rate? What about different kinds of interest rates? Mortgage rates are different from credit card rates which are different from government bond yields. Why? How exactly do interest rates affect the economy? Sure, they make borrowing more or less expensive, but do they do anything else? How do banks play into all of this? The Fed is also a lender of last resort. What does that mean? These questions and more are what I’ll attempt to answer with this series of blog posts. Let’s start with the mechanics.

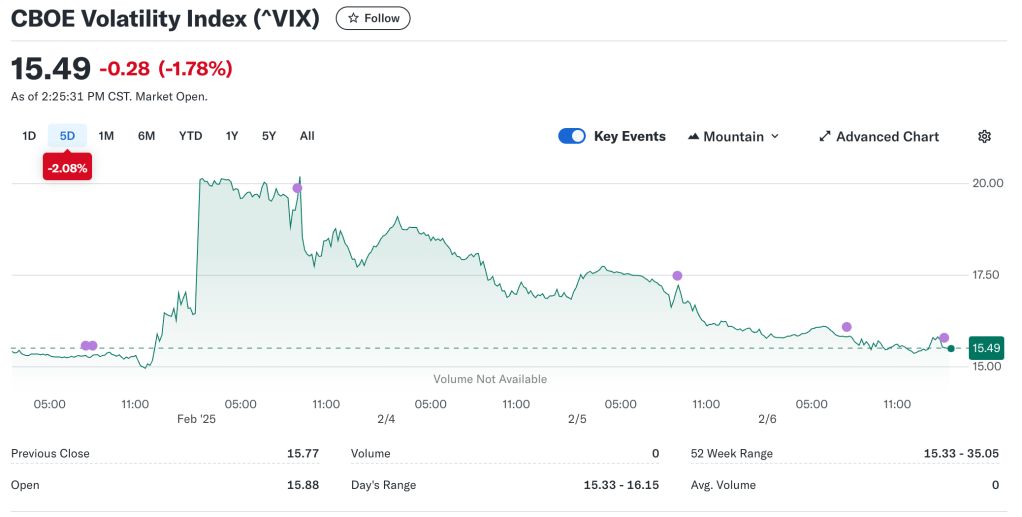

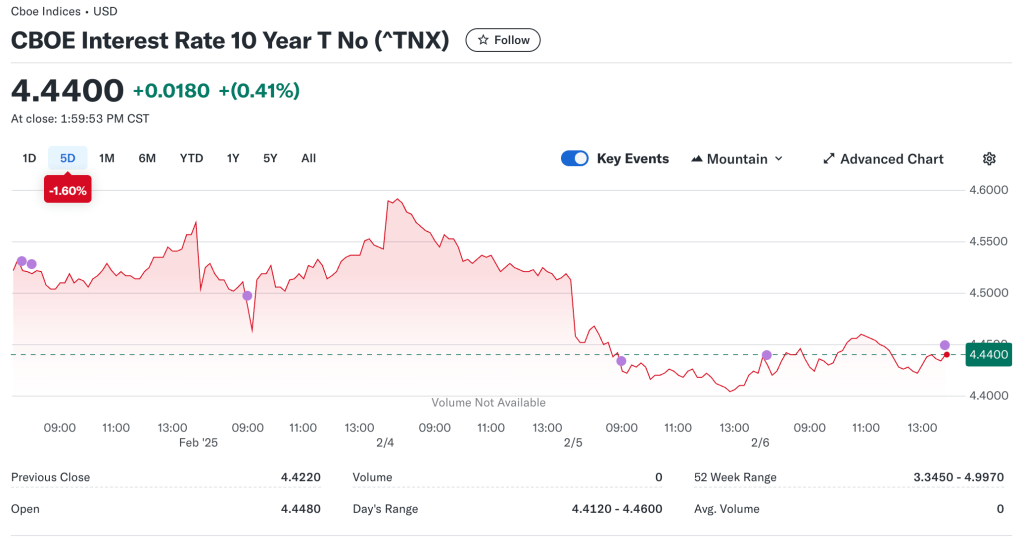

Okay, sweet. The proposed 25% tariffs on all Mexican and Canadian goods (with carve-outs for Canadian energy) were postponed by a month. This is undoubtedly good news. To Trump’s credit, he was able to get seeming concessions from our neighbors. He first called Mexican President Claudia Sheinbaum wherein she agreed to send thousands of troops to the border to help curb illegal immigration and the smuggling of fentanyl. In return, the US vowed to help limit the amount of guns funneling into Mexico. Similarly, Trump called Canadian Prime Minister Justin Trudeau striking a deal to delay the tariffs. Trudeau promised to “ensure 24/7 eyes on the border” (to deal with the ‘problem’ of fentanyl from the northern border) and pledged $1.3 billion to that end, as well as agreeing to a US-Canada joint strike force to tackle organized crime. The CBOE volatility index initially jumped slightly as we approached implementation but has since tapered off – so too have long-term interest rates. This reversion reflects the general sentiment of the situation – crisis averted, at least for now.

Volatility spiked when tariffs seemed likely to be implemented, dipped when deals with Mexico and Canada were reached. Data source: Yahoo Finance10-year Treasury yields followed the same pattern. Data source: Yahoo Finance

The long-term implications of these last-minute deals are unclear. Now that Trump has succeeded in scaring Mexico and Canada into an agreement, will he become more emboldened next time around? As the tariff moratorium comes to a close, will he demand even more from other countries? How much are these countries willing to take? I’m not going to pretend to know what Trump is going to do. However, given that he just implemented 10% tariffs on all Chinese imports, I think the probability of future tariffs is significant. And, even though tariffs on Mexico and Canada were delayed, there was an excellent Bloomberg piece claiming that Mexico in particular is hurt by these threats even if they aren’t executed. The extent of the pain is decidedly mitigated, but the incentive to funnel foreign direct investment and resources into Mexico is diminished with the threat of tariffs and the deterioration of the US-Mexico-Canada (USMCA) agreement. Regardless, let’s talk more about the tariffs on China.

There is a significant imbalance between the magnitude of the US and China’s tariffs. The US placed 10% tariffs on China across the board. This affects $525 billion of US imports, which accounts for ~14% of Chinese exports and ~3% of their total GDP. Conversely, China assumed a more tepid approach, placing 10-15% levies on roughly 80 US energy products and agricultural tools. These affect $14B of imports, account for 0.72% of US imports and 0.05% of total GDP (import data from Bloomberg, who sourced it from China Customs). China also added export restrictions on tungsten and other metals predominantly used in the electronic, aviation, and defense industries. In sum, the US is taxing China far more than China is taxing the US. As far as China’s response goes, their export restrictions will likely hamper production in the aforementioned industries while their tariffs should increase prices by a small but unknown magnitude. How much? I don’t know but it doesn’t seem like a drastic effect. Nonetheless, if this trade war continues to escalate, these effects will decidedly be felt by the everyday consumer.

The tariffs that the US erected are a different, more consequential story. China’s response was measured and relatively light, thus the expected drag on growth should be tame. The lack of tariffs keeps the average price level of US goods and services roughly constant, neither incentivizing nor disincentivizing the purchase of exports. However, our decision to impose tariffs should increase the prices of Chinese exports by a non-negligible amount. As stated, the US is applying 10% tariffs on 14% of our total imports. This is crazy. How much do these price increases matter? As shown below, both headline and core PCE inflation have been hovering somewhat near the Federal Reserve’s 2% target, with core inflation stagnating in recent months and headline increasing.

Progress towards the Fed’s 2% inflation target has stalled. Tariffs may force them to keep rates high. Data source: FRED

Anything that risks increasing inflation – in our case, tariffs on China increasing prices – pressures the Federal Reserve to keep rates higher for longer. Core inflation holding steady implies the underlying, persistent rate of price increases (removing the typically volatile food and energy components) is growing at a steady pace. The Federal Reserve wants to see more progress towards its target but is in a state of limbo. As Federal Reserve President Jerome Powell stated in his Jan 29 press conference, “Inflation has moved much closer to our 2 percent longer-run goal, though it remains somewhat elevated… the Federal Open Market Committee decided to leave our policy interest rate unchanged and to continue to reduce our securities holdings.” That is, they have decided to keep short-term interest rates constant while continuing to engage in quantitative tightening. If tariff-induced inflation becomes a significant problem, Powell and co. will be forced to keep rates high to keep the economy from overheating and inflation from spiraling.

What I’m getting at is simple: not only will these tariffs increase inflation, but also interest rates by way of expectations of the Federal Reserve. If credit card APR, mortgage rates, auto loans, any other variable loan, or wealth discounting matters to you, then Trump’s tariffs hurt you. The extent of this hurt is controlled for now but might expand in the future.

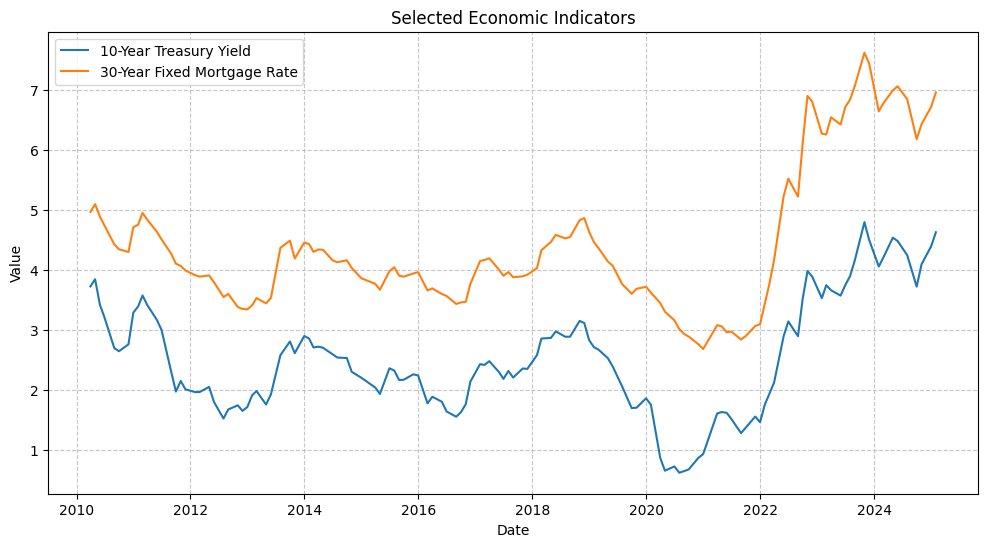

Long-term interest rates, including 30-year fixed mortgage rates, are near a two-decade high. Trump’s tariffs reduce the probability of these rates ‘normalizing’ soon. Data source: FRED

The biggest story of the day appears to be the incipient stages of a trade war between the US, Mexico, and Canada (I don’t believe any tariffs are being planned between Canada and Mexico, though). Trump is allegedly imposing these tariffs in response to excess drug/opiate smuggling and illegal immigration. Assuming this is justified, I don’t particularly see why Canada finds itself at Trump’s mercy. From what I understand, many of the intermediate inputs of dangerous drugs like opioids are legally imported from East Asia to Mexico, assembled there, and then illegally smuggled across the border. This is a problem. I ought to do more research into how this issue could be solved. What can US Customs & Border Patrol do? What about Mexican authorities? Chinese authorities (assuming East Asia = China)? Regardless, it doesn’t seem to be Canada’s fault.

If actually imposed (slated for Tuesday, the 4th), these tariffs will have a couple of domestic economic effects. First, USimports from both countries will become more expensive. A first-order effect would imply that 25% tariffs across the board should raise prices by around 25%. I don’t know if this will actually hold true. Consider this example:

Suppose exporting firms in Canada and Mexico have some degree of price-setting power. That is, they are currently charging above their marginal cost and can lower their price, or they can lower their price below marginal cost because they expect future rewards with increased market share. Then, these firms may lower the sticker prices of their goods and services to sell more. That is, if prices are 100% sticker with 0% tax ex-ante, ex-post prices may be 90% sticker with 25% tax for a total of 115%. A 15% increase (which, conspicuously, is lower than 25%). This depends on how much market power these firms have and the perceived importance of market share (which goes hand-in-hand with the perceived duration of tariffs. If a firm believes tariffs are short-lived, they may want to lower prices for more market share to benefit when tariffs evaporate and would be willing to operate at a loss).

Another domestic effect (and the seeming economic rationale) is protectionism. By taxing firms that are exporting to the US and increasing their prices, domestic firms in competition with foreign firms benefit. Suppose we go from a 0% tax on Canadian cars to a 25% tax. We likely see a price increase for the reasons listed above. Purchases of domestic cars, on the other hand, are not ~25% more expensive. Thus, domestic cars seem much more attractive, people buy more, and these firms are better off. These firms pay their employees income, so domestic income increases. As incomes increase, spending increases. And, since one person’s spending is another’s income, incomes across the board increase (this income effect may be relatively small, but overall good for Americans).

However, this assumes that we are only taxing final goods. I don’t know the exact details of these tariffs – maybe it is the case that 25% across the board refers to final goods (probably not, though). Let’s strip away this assumption. 25% means 25%. We aren’t just taxing Canadian cars at 25%. We’re taxing their steel, aluminum, electronics, microchips, and all the other intermediate goods that we use to construct a car. In this scenario, the price of domestic cars rises as well! The price probably won’t rise as much as foreign cars (because I’m assuming every factor of production in car assembly isn’t imported and taxed. If every part was imported and taxed, labor costs aside, prices should rise in tandem). Nonetheless, Domestic prices still probably rise. Then, the effects on domestic firms are ambiguous. On the one hand, they capture more demand from foreign firms because foreign firms now have higher prices. On the other hand, production is now more costly as intermediate inputs are taxed and more expensive, raising the price, and reducing demand for these domestic firms. This probably nets positive for the domestic firms, but perhaps that’s just me spitballing.

Everything I just mentioned is a first-order effect. We tax Mexico and Canada, they don’t tax us. In reality, it only seems logical that Canada and Mexico would respond with tariffs in turn. And, it seems that these countries are already planning retaliatory targeted tariffs. So, suppose Mexico and Canada levy 25% tariffs on American goods and services. Then, flip all the effects I previously laid out and add them. American goods become more expensive for foreign consumers. We lose their business. Domestic firms lose money, pay less income to employees, they spend less, resulting in less spending/income in the US. This doesn’t seem great for the US. It is this retaliatory effect that appears to have so many economists concerned about a destabilizing trade war.

I’m glossing over much of the nuance involved in these tariffs. I failed to account for three main forces: game theory, foreign exchange effects, and budget deficit effects. Game theory applies because it could be the case that tariffs are being used to ‘bully’ other nations into submission. And, if successful, America could accomplish other economic and non-economic goals with the threat of tariffs alone. These goals include limiting immigration and drugs, the purchase of Greenland, renaming the Gulf of Mexico, etc. Also, if Trump can implement relatively smaller tariffs and prevent retaliation (which seems unlikely), these tariffs could truly help the American people. I have also ignored the foreign exchange rate in this analysis. In short, USD should appreciate as relative demand for peso and Canadian Dollar fall. Demand for these currencies fall because exports to US account for more of MEX and CAN economy than exports from US to MEX and CAN matter for the American economy. Thus, a greater proportion of MEX and CAN’s output is slapped with tariffs and see reduced demand for their currency. This is corroborated by Bloomberg’s report that USD and oil jumped. Further, I have ignored the effect on the budget deficit (increased tax revenue should decrease the deficit).

Although I could enrich my prior analysis with these omitted variables, I think the general effect remains the same: unless Trump forces heavy concessions and prevents retaliation, these tariffs will hurt the American people. At this moment, it seems unlikely Trump can accomplish that. Maybe that changes, and if so I’ll write about it. It also seems very likely that America’s trading partners will suffer from these tariffs.

Hi! My name is Andrew Robinson. I’m a senior at Harvard studying Economics with honors. I’m originally from Athens, Georgia, where I lived for 18 years with my mom, dad, and older brother.

I’ve found myself with some free time senior year, and want to use this opportunity to learn and write about the world around me. With that said, here’s a little more in terms of a background.

My parents are both staunch Democrats (MSNBC hosts occupied our TV most evenings growing up). My brother, quite possibly the most politically interested individual on the planet, has a strong left-wing lean as well. To no one’s surprise, my political beliefs are generally progressive, but with no strong convictions. This is quite different from a few years ago — I was very opinionated with rather extreme opinions when I matriculated to Harvard. I explored far-left political content online and read works by Marx, Engels, and other socialist and communist thinkers. I viewed capitalism through a lens of class struggle, believing that a dominant capitalist class exerted control over the working class in a strict and exploitative manner.

Since college, though, I’ve realized how complicated this world is. I’ve become much more sparing with my opinions, particularly the political ones. Having opinions about consequential problems, issues, and topics is important, though. I want to become opinionated again, but I want to do it the right way. I plan on using this blog as a commitment device. Here, I will explore topics ranging from politics, economics, finance, AI, and more. I want to engage every topic in good faith and with an open mind. Given sufficient evidence, I am always willing to change my mind. If it appears I’ve made a mistake (factual or otherwise) on this site, please let me know!